Have you ever wondered about the individuals who shape the landscape of the insurance industry? Anthony Martin is one such figure, renowned for his contributions to the world of final expense insurance. With a career spanning over 20 years, Anthony’s journey is as inspiring as it is insightful. From humble beginnings to becoming a trusted advisor, his story is a testament to hard work, dedication, and a passion for helping others. In this blog post, we will go through Anthony Martin Final Expense experience, his biography and his success story, exploring the key moments that have defined his career and the principles that have guided his success. Let’s explore together! Who is Anthony Martin? Anthony Martin is a prominent figure in the insurance industry, known for his exceptional achievements and contributions. As the founder, CEO, and owner of Choice Mutual, he has established himself as a leader in the field of final expense insurance. Anthony Martin’s Final Expense journey began in 2010 when he became a licensed insurance agent, and since then, he has held an active insurance license in all 50 U.S. states, including Washington, DC. One of Anthony’s remarkable accomplishments is being recognized as the No. 1 top-producing agent for simplified issue life insurance with Mutual of Omaha for four consecutive years from 2018 to 2021. His dedication to excellence has also been acknowledged by Aetna, naming him its No. 1 life agent for 2020. Moreover, Anthony’s commitment to professionalism and expertise is evident in his qualification as a non-member of MDRT since 2017, a prestigious honor within the life insurance trade organization in the U.S. Anthony Martin’s Life History Let’s have a closer at Anthony Martin Final Expense history and major life achievements: Education Anthony Martin’s path to becoming a prominent figure in the insurance industry started with his early life and education. While specific details about his early years are limited, it is known that he valued continuous learning. His educational background provided him with the foundational knowledge that later contributed to his success in the insurance industry. Career Beginning In 2010, Anthony officially entered the insurance field as a licensed insurance agent. This marked the beginning of a career that would soon make him a leader in the final expense insurance market. His early days likely involved overcoming challenges and gaining hands-on experience, setting the stage for his future accomplishments. Start of Choice Mutual The turning point in Anthony’s career came with the founding of Choice Mutual, an insurance agency that became known for excellence in the final expense sector. As the founder, CEO, and owner of Choice Mutual, Anthony took on a leadership role that allowed him to shape the company’s values and strategies. Achievements Anthony’s exceptional achievements as a life insurance agent did not go unnoticed. His consistent ranking as the No. 1 top-producing agent for simplified issue life insurance with Mutual of Omaha from 2018 to 2021 showcased his remarkable success. Aetna’s recognition of him as the No. 1 life agent in 2020 further highlighted his impact on the industry. Leader of Major Insurance Providers Beyond selling policies, Anthony’s expertise led major insurance companies such as Mutual of Omaha, Aetna, and Royal Neighbors of America to seek his advice for product development. His involvement in shaping and enhancing insurance products and application processes demonstrated his influence on a national scale, benefiting millions of Americans. Publications and Conferences As a recognized life insurance expert, Anthony’s insights have been featured in prestigious publications like Forbes, Investopedia, and CNBC. He is also a sought-after speaker at industry conferences, where he shares his knowledge and expertise with a wider audience. Member of Professional Groups Anthony’s standing in the industry is reflected in his membership in exclusive professional groups such as the Forbes Finance Council, Entrepreneur.com Leadership Network Contributor, and Newsweek Expert Forum. These memberships affirm his track record of success and leadership within the financial and insurance sectors. Anthony Martin’s biography is a testament to his journey from a licensed insurance agent to a respected figure in the final expense insurance market. His story is one of continuous learning, resilience in the face of challenges, and a commitment to excellence that has made a lasting impact on the insurance industry. How Anthony Martin Made One Million in Final Expenses? Anthony Martin final expense’s success comes through a combination of hard work, dedication, and strategic planning. Here’s how he made one million in final expense: 1- Building Expertise Anthony invested time and effort into becoming an expert in the final expense insurance market. He familiarized himself with the needs of his target demographic. And gained a deep understanding of the products and services available in the industry. 2- Client-Centric Approach Anthony prioritized his clients’ needs above all else. By taking the time to listen to their concerns and providing personalized solutions, he built trust and loyalty, leading to repeat business and referrals. 3- Strategic Partnerships Anthony forged strategic partnerships with major insurance companies such as Mutual of Omaha and Aetna. These partnerships allowed him to offer a wide range of products and services to his clients, increasing his earning potential. 4- Consistent Performance Anthony consistently ranked as the top-producing agent for simplified issue life insurance. Mutual of Omaha and received recognition from Aetna as the No. 1 life agent. His consistent performance and track record of success contributed to his ability to earn one million in final expense. 5- Innovation and Adaptation Anthony demonstrated a willingness to innovate and adapt to changing market conditions. He leveraged technology to streamline processes, improve efficiency, and enhance the customer experience, ultimately increasing his earning potential. 6- Community Engagement Anthony actively engaged with his community and built strong relationships with local businesses and organizations. By giving back and supporting causes that were important to his clients, he solidified his reputation as a trusted advisor and community leader. Therefore, Anthony Martin final expense insurance’s success can be attributed to his expertise, client-centric approach, strategic partnerships, consistent performance, innovation, and community engagement.

Survivor Benefit Plan vs Life Insurance: A Military Comparison

Are you weighing your options between the Survivor Benefit Plan (SBP) and life insurance as a military member? Deciding how to protect your loved ones financially is a critical decision, and understanding the differences Survivor Benefit Plan vs Life Insurance. The Survivor Benefit Plan (SBP) offers a monthly annuity to eligible beneficiaries, while life insurance provides a lump-sum payment. Each option has its own set of considerations, including cost, flexibility, and portability. In this comprehensive guide, we’ll compare the Survivor Benefit Plan vs life insurance to help you make an informed decision. Whether you’re a service member nearing retirement or a spouse seeking financial security, this comparison will provide valuable insights into choosing the right option for you and your family’s future. What is the Survivor Benefit Plan (SBP)? The Survivor Benefit Plan (SBP) is a program the Department of Defense offers for military retirees. It provides eligible beneficiaries with a monthly payment upon the retiree’s death, serving as a form of continued income to support surviving spouses or dependents. This payment is designed to help offset the loss of income that occurs when a military retiree passes away. The SBP is an important financial planning tool for military families, offering a measure of security and peace of mind knowing that their loved ones will have some financial support in the event of their death. Understanding Life Insurance Life insurance is a contract between an individual and an insurance company. In exchange for regular premium payments, the insurer agrees to provide a lump-sum payment, known as a death benefit, to the designated beneficiaries upon the insured’s death. This payment is intended to provide financial security to the insured’s loved ones, helping them cover expenses such as funeral costs, mortgage payments, and living expenses. There are several types of life insurance, including term life insurance, which provides coverage for a specific period, and permanent life insurance, which provides coverage for the insured’s entire life as long as premiums are paid. Life insurance can be an essential part of a financial plan, offering protection and peace of mind to policyholders and their families. Survivor Benefit Plan vs Life Insurance: Coverage Comparison When comparing the Survivor Benefit Plan vs life insurance, it’s essential to understand the coverage differences each option offers: Survivor Benefit Plan (SBP) 1- Monthly Annuity SBP provides eligible beneficiaries with a monthly payment upon the death of a military retiree. This payment serves as a form of continued income to support surviving spouses or dependent children. 2- Coverage Extension SBP coverage extends to surviving spouses and dependent children, offering financial protection to eligible family members. 3- Premium Deduction Premiums for SBP are deducted from the retiree’s monthly pension, reducing the amount received but ensuring continuous coverage for beneficiaries. 4- Cost-of-Living Adjustments SBP payments are subject to cost-of-living adjustments, potentially increasing over time to keep pace with inflation. 5- Benefit Reduction Benefits under SBP may be reduced if the beneficiary receives other benefits, such as Dependency and Indemnity Compensation (DIC). Life Insurance 1- Lump-Sum Payment Life insurance provides a lump-sum payment to designated beneficiaries upon the insured’s death, offering financial protection in the form of a single payout. 2- Coverage Determination The coverage amount for life insurance is determined by the policyholder’s chosen coverage level, offering flexibility to tailor the amount of protection based on individual needs. 3- Premium Payment Premiums for life insurance are paid directly by the policyholder, separate from any pension or other income sources. 4- Policy Terms Policy terms and coverage options vary among insurers, allowing individuals to select the policy that best fits their financial situation and goals. 5- Benefit Stability Benefits from life insurance policies are typically not subject to reductions based on other benefits received, providing stable financial protection to beneficiaries. While both SBP and life insurance offer valuable coverage, they differ in their payment structures, coverage extensions, premium arrangements, and benefit stability. Understanding these differences is crucial for military personnel and their families when making decisions about financial planning and protection. Survivor Benefit Plan vs Life Insurance: Cost Considerations When comparing the Survivor Benefit Plan vs life insurance, it’s vital to consider the cost implications associated with each option. Here’s a comparison table highlighting the key cost considerations between the Survivor Benefit Plan (SBP) and life insurance: Cost Consideration Survivor Benefit Plan (SBP) Life Insurance Premium Payment Deducted from retiree’s pension Paid directly by the policyholder Cost Variation Based on coverage level, beneficiary designation Based on age, health, coverage amount Cost-of-Living Adjustments Payments subject to adjustments Premiums may increase over time Impact on Income Reduces retiree’s disposable income Requires budgeting for premiums Flexibility Limited flexibility in premium payment options Flexible premium payment options Please note that the actual costs and benefits may vary based on individual circumstances and policy details. Moreover, both the Survivor Benefit Plan vs life insurance have associated costs that retirees need to consider. SBP offers the convenience of premium deduction from the pension but may result in a reduced monthly income. On the other hand, life insurance requires direct premium payment but offers flexibility in coverage options and may be more cost-effective for certain individuals depending on their age, health, and coverage needs. Survivor Benefit Plan vs Term Life Insurance: Compare the Options Choosing between the Survivor Benefit Plan (SBP) and term life insurance is a critical decision for military families. Each option offers unique benefits and serves different financial protection needs. When deciding between the Survivor Benefit Plan (SBP) and term life insurance, consider the following factors: 1- Purpose of Coverage: 2- Coverage Duration: 3- Cost: 4- Flexibility: 5- Long-Term Planning: Ultimately, the choice between SBP and term life insurance depends on your specific circumstances, financial goals, and the needs of your beneficiaries. Consulting with a financial advisor can help you make an informed decision based on your unique situation. Military Survivor Benefit Plan vs Life Insurance: Which One is Best? Deciding between the Survivor Benefit Plan vs life insurance ultimately depends on your circumstances, preferences, and

OpenCare Final Expense Insurance: Ensuring Peace of Mind

End-of-life expenses are a sensitive topic, but it’s important to talk about. Providing funds to your dependents to cover funeral and other end-of-life expenditures after your death is the fundamental concept of an OpenCare Final Expense Insurance: Ensuring Peace of Mind plan. These arrangements are fantastic for people who want to avoid burdening their families with excessive funeral costs. In addition, they let you set the price of your plan and the amount that will be paid to your beneficiaries. OpenCare Final Expense Insurance Plan is not just a solution; it’s a commitment to providing comprehensive coverage that addresses your unique needs and safeguards your legacy. As you navigate life’s uncertainties, have you pondered a plan that covers final expenses and offers a personalized touch to match your lifestyle and preferences? OpenCare goes beyond a one-size-fits-all approach, allowing you to tailor your plan to reflect your circumstances. How can you protect your loved ones from the financial burden of final expenses? Can your plan be customized to align with your distinct aspirations? Does it Sounds interesting? Here is a comprehensive explanation of open care final expense plans and how they operate. Okay, let’s get started. How do open care final expense plans work? OpenCare Final Expense Insurance Plans are designed to provide individuals and their families with financial security during a challenging time. Here’s an overview of how OpenCare Plans work: Application Process: The process typically begins with filling out an application. During this stage, individuals provide information about their health, lifestyle, and other relevant details. OpenCare aims to make this step straightforward and accessible, ensuring applicants can easily navigate the application process. Underwriting and Approval: OpenCare conducts an underwriting process to assess the applicant’s insurability. This may involve reviewing medical records, answering health-related questions, and sometimes undergoing a medical examination. Once the underwriting process is complete, the applicant is notified of their approval status. Policy Customization: OpenCare Expense Plans offer a degree of customization to align with individual needs. Policyholders can often choose the coverage amount that suits their financial goals and family’s needs. This customization ensures the plan is tailored to address specific concerns, such as funeral expenses, medical bills, or outstanding debts. Premium Payments: Policyholders are required to make regular premium payments to keep the OpenCare Expense Plan active. Premiums can typically be paid monthly or annually, allowing individuals to choose a payment schedule that fits their budget. Beneficiary Designation: During the application process, individuals designate beneficiaries who will receive the death benefit upon the policyholder’s passing. This benefit is intended to cover final expenses, ensuring that loved ones are not burdened with the financial costs associated with end-of-life arrangements. Coverage Activation: Once the policy is approved and the initial premium is paid, the OpenCare Final Expense Plan becomes active. This means that the policyholder is now covered, and in the event of their passing, the designated beneficiaries will receive the agreed-upon death benefit. Claim Process: When the policyholder passes away, the designated beneficiaries or their representatives initiate the claims process by contacting OpenCare. The necessary documentation is submitted, and the death benefit is disbursed to the beneficiaries upon approval. This money can cover funeral expenses, medical bills, or other financial obligations. OpenCare Plans aim to simplify securing financial protection for end-of-life expenses, providing individuals and their families with a thoughtful and customizable solution. It’s crucial for applicants to thoroughly understand the terms and conditions of their chosen plan and consult with OpenCare representatives to ensure their specific needs are met. How much are open care life insurance plans? The cost of a monthly $8,000 policy using Open Care will range between $17 and $252, based on their website. Your actual premium will depend on several elements, which include your age, your health status, whether you smoke, and how much coverage you are interested in getting. The average final expense policy with a benefit amount of $10,000 can be as low as $50 to $100 per month, depending on the insurance and your personal factors. Here’s a breakdown of estimated monthly premiums for an $8,000 burial insurance policy, according to Open Care’s website: AGE Male Non-Smoker Male Smoker Female Non-Smoker Female Smoker 40 $19 $24 $17 $21 50 $25 $33 $21 $27 60 $36 $51 $29 $39 70 $60 $94 $42 $59 80 $111 $167 $84 $102 90 $242 $252 $205 $229 Benefits of Open Care Final Expense Plans OpenCare Final Expense Plans offer a range of benefits beyond addressing immediate financial concerns, providing peace of mind for individuals and their families during challenging times. Here are some key advantages of choosing OpenCare Final Expense Plans: Financial Security for Loved Ones: The primary benefit is the assurance that your loved ones will be financially supported in the event of your passing. The death benefit provided by the plan can be used to cover funeral expenses, medical bills, outstanding debts, or any other financial obligations, alleviating the burden on family members during an emotionally challenging period. Customizable Coverage: OpenCare understands that every individual’s situation is unique. With the ability to customize coverage amounts, policyholders can tailor their Final Expense Plan to match their financial goals and family needs. This flexibility ensures that the plan is as individualized as the lives it aims to protect. Accessible Application Process: OpenCare strives to make the application process simple and accessible. With user-friendly forms and a commitment to transparency, individuals can easily navigate the application process, ensuring that obtaining coverage is a straightforward and hassle-free experience. Affordable Premiums: OpenCare Final Expense typically comes with affordable premium options, allowing individuals to choose a payment plan that aligns with their budget. This affordability ensures that financial protection is within reach for many individuals, regardless of their financial circumstances. No Medical Exam Option: OpenCare often provides options for individuals who prefer to avoid a medical examination during the underwriting process. This feature can benefit those with pre-existing health conditions or seeking a quicker approval process. Flexible-Premium Payment Options: OpenCare Final Plans usually offer flexible

Is Cremation Cheaper Than Burial? Compare Affordable Options

In this blog post, we’ll discover is cremation cheaper than burial by breaking down each into simple terms. The choice can be emotionally challenging and financially significant. Many people find themselves wondering which option is more cost-effective. The short answer is often cremation, but the full story is more complex. What happens when it’s time to decide between cremation and burial? We’ll also look at additional factors like environmental impact and personal preferences. Whether you’re planning ahead or making decisions in a time of need, this guide will provide valuable insights to help you choose the best option for your circumstances. Let’s explore the details of cremation and burial to find out which option might be best for you. Understanding the Basics When considering end-of-life options, it’s essential to understand what cremation and burial involve. Each has its unique processes, services, and products that contribute to the overall cost and experience. What Is Cremation? Cremation is the process of reducing a body to ashes using high temperatures. After the cremation, the ashes, or “cremains,” can be kept in an urn, scattered, or buried. This method is often chosen for its simplicity and flexibility. What Is Burial? Burial involves placing the body in a casket and interring it in the ground. This process often includes purchasing a burial plot, a casket, and a headstone or grave marker. Burials can take place in cemeteries or on private land, depending on local regulations and personal preferences. Is Cremation Cheaper Than Burial? Yes, cremation is typically cheaper than burial. However, the cost difference depends on various factors such as the type of services chosen, location, and personal preferences. In most cases, direct cremation tends to be the most affordable option, with costs ranging from $500 to $3,000. Traditional cremation services can be more expensive, ranging from $2,000 to $7,000. On the other hand, burial costs can range from $1,000 to $4,000 for a direct burial and $7,000 to $12,000 or more for a traditional burial. Factors like location, service choices, and personal preferences can influence the final costs. Ultimately, individuals should consider these factors carefully to make an informed decision that aligns with their budget and preferences. Cost Breakdown: Cremation vs. Burial Having an idea about the costs associated with cremation and burial can help you make an informed decision. Here’s a detailed breakdown of the expenses for each option. 1- Direct Cremation Costs Direct cremation is the most straightforward and cost-effective option, typically ranging from $500 to $3,000. Here’s what you can expect to pay for: 2- Traditional Cremation Costs Traditional cremation involves additional services like a viewing or ceremony, which increases the cost to between $2,000 and $7,000. These costs include: 1- Direct Burial Costs A direct burial skips the ceremony and involves placing the body directly in the ground. This typically costs between $1,000 and $4,000. The expenses include: 2- Traditional Burial Costs Traditional burials are more elaborate, with costs ranging from $7,000 to $12,000 or more. These costs encompass: Factors Influencing Costs of Cremation vs. Burial Understanding the cost differences between cremation and burial involves looking at several factors that can influence the overall expenses. Here, we’ll explore key elements that affect the costs associated with each option. 1- Location The geographical location where the services are provided significantly impacts the cost of both cremation and burial. Urban areas generally have higher costs due to increased demand and higher operational expenses. In contrast, rural areas often have lower costs because of the lower demand and cheaper land prices. 2- Service Choices The specific services you choose will greatly influence the overall cost of cremation or burial. Direct Cremation/Burial skips the ceremonial aspects and focuses solely on the cremation or burial process. It’s typically the most cost-effective choice, as it eliminates expenses related to viewings, ceremonies, and additional transportation. 3- Additional Services Additional services such as memorial services, floral arrangements, and obituary notices can add to the cost. The more elaborate the services, the higher the overall expense will be. Moreover, your personal choices, including the type of casket or urn and other memorial items, can also impact the cost. 4- Transportation The cost of transporting the body from the place of death to the funeral home, crematorium, or burial site can vary. Local transportation costs are generally lower, but they can still add up, especially if multiple transfers are required. If the body needs to be transported over a long distance, such as across states or internationally, the costs can be substantial. Environmental Considerations Cost isn’t the only factor to consider. Many people are also concerned about the environmental impact. Cremation does produce emissions, including carbon dioxide. However, modern crematoriums are increasingly using cleaner, more efficient technologies. Burial involves the use of land, which can be a concern in crowded urban areas. Traditional burials also use chemicals for embalming, which can leach into the ground. Personal and Cultural Factors Deciding between cremation and burial is also influenced by personal, cultural, and religious beliefs. Some religions have specific requirements for handling the deceased. For example, traditional Jewish and Muslim practices prefer burial. Many people have strong personal feelings about how they want to be remembered. Some may find comfort in the idea of a burial site, while others prefer the simplicity of cremation. Why Cremation Is Often Cheaper? Cremation is often considered a more affordable option compared to traditional burial for several reasons. Cremation typically involves fewer services than burial. With direct cremation, for example, there’s no need for embalming, a casket, or a burial plot. This reduction in services means fewer expenses, resulting in lower overall costs. The cremation process itself is simpler and requires fewer resources than burial. There’s no need for elaborate funeral services or preparations. Direct cremation, in particular, involves minimal procedures, such as transportation and cremation, leading to lower costs. Cremation offers more flexibility in timing. Families can choose to hold a memorial service at a later date, allowing them to shop around for affordable

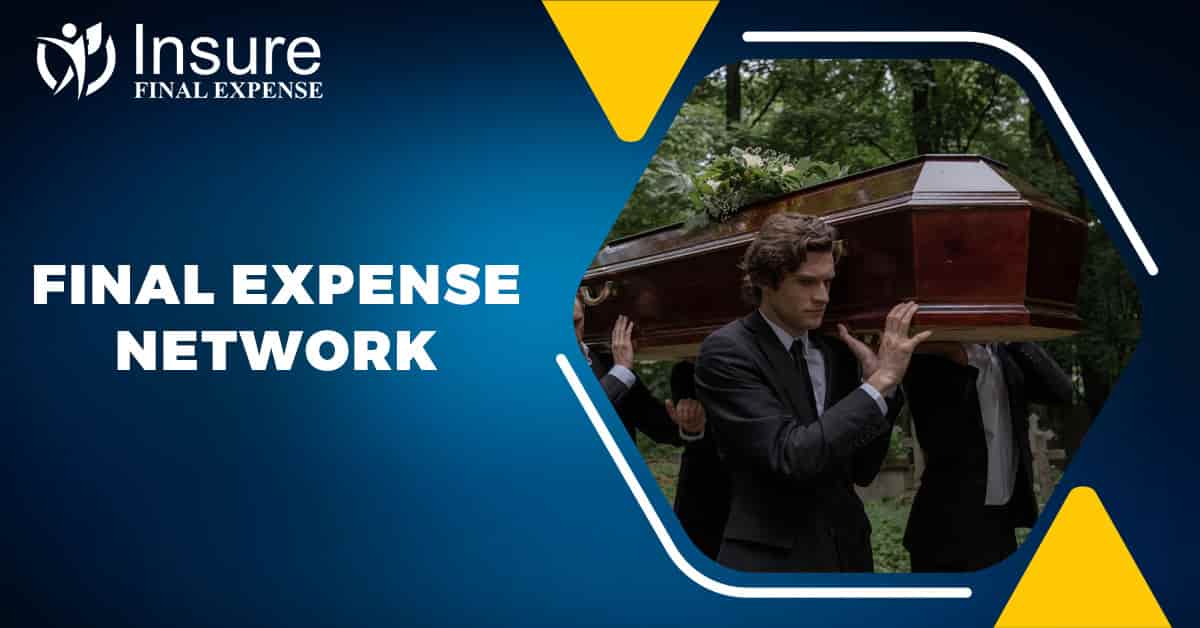

Final Expense Network: Reviews, Wholesale, & Commercial Info

Are you prepared for the certain expenses that come with the end of life? Final expenses can be a burden on your loved ones, but with the right planning, you can ease their financial worries. Final Expense Network offers solutions to help you prepare for these costs, whether you’re an individual looking for coverage or a broker seeking wholesale options. In this guide, we’ll explore the world of this insurance company, from reviews of their services to wholesale and commercial information. You’ll also discover its plan, services and why this network is a top choice for final expense insurance. But let’s start with some basic information! What is the Final Expense Network? The Final Expense Network is a leading provider of final expense insurance solutions. They offer a range of products personalized to meet the needs of individuals and families facing end-of-life expenses. With a focus on customer service and value, the company has built a reputation for excellence in the industry. Final expense insurance, also known as burial or funeral insurance, is designed to cover the costs associated with a funeral and other end-of-life expenses. These costs can include funeral services, burial or cremation, and other related expenses. By purchasing final expense insurance, individuals can ensure that their loved ones are not burdened with these costs during an already difficult time. Final or Funeral Expense Network offers a variety of final expense insurance products to meet the needs of different individuals and families. These products typically have simplified underwriting processes, making them accessible to a wide range of applicants. Additionally, it provides personalized customer service to help clients choose the right coverage for their needs. Final Expense Network Plan The plan offers a comprehensive solution to cover the expenses that arise at the end of life. It’s crafted to give individuals and their families financial protection and peace of mind during a tough period. Key Features of the Final Expense Network Plan: This plan is flexible, allowing individuals to customize coverage amounts to match their specific needs. Whether it’s covering funeral costs, burial expenses, medical bills, or outstanding debts, the plan can be personalized accordingly. Applying for the plan is straightforward. Unlike some insurance plans, it doesn’t typically require extensive medical examinations or background checks, making it more accessible to individuals seeking coverage. When the policyholder passes away, the benefits from the plan are usually paid directly to the designated beneficiary. This swift disbursement ensures that funds are available promptly to cover necessary expenses, providing crucial financial support during a difficult time. The company offers various plan options, allowing individuals to choose features and benefits that suit their preferences and financial situation. These options can include different coverage levels, premium payment schedules, and additional riders for extra protection. Moreover, this insurer’s plan is a reliable and adaptable solution designed to address the specific financial needs related to one’s final expenses, offering reassurance and support for family members during a challenging time. Services of Final Expense Network It offers a range of services tailored to meet the needs of individuals and families facing end-of-life expenses. Their services include: 1- Insurance Products It offers a variety of final expense insurance products designed to provide financial protection for end-of-life expenses. These products typically include coverage for funeral services, burial or cremation costs, and other related expenses. 2- Simplified Underwriting The insurance products of this insurance company often feature simplified underwriting processes, making it easier for individuals to qualify for coverage. This is especially beneficial for individuals with pre-existing health conditions or other factors that may affect their insurability. 3- Flexible Payment Options Their insurance products typically come with flexible payment options, allowing individuals to choose a payment schedule that works for their budget. Personalized Customer Service The insurance company prides itself on its personalized customer service, helping clients choose the right coverage for their needs and providing support throughout the claims process. Overall, Final Expense Network is a trusted provider of final expense insurance solutions, offering comprehensive coverage and personalized service to help individuals and families prepare for the financial challenges of end-of-life expenses. Benefits and Drawbacks of Final Expense Network The company comes with several benefits, but it also has some drawbacks. Let’s explore both sides: Benefits Drawbacks So, the company offers valuable benefits such as financial protection and simplified underwriting, but it also has drawbacks such as limited coverage options and higher premiums. It’s important to carefully weigh these factors and consider your individual needs when choosing an insurance provider. Average Cost of Final Expense Network in the USA The average cost of this plan in the USA can vary based on several factors, including the individual’s age, health status, coverage amount, and the specific plan chosen. However, on average, final expense insurance policies typically range from $30 to $100 per month. For example, a healthy 50-year-old individual might pay around $30 to $50 per month for a final expense insurance policy with a coverage amount of $10,000 to $20,000. On the other hand, a 70-year-old individual with health issues might pay closer to $70 to $100 per month for the same coverage amount. It’s important to note that these are just rough estimates, and the actual cost can vary significantly based on individual circumstances and the specific details of the policy. It’s always best to get a personalized quote from Final Expense Network or another insurance provider to get an accurate idea of the cost for your specific situation. Reviews of Final Expense Network The company mostly has positive reviews from its satisfied customers. Here we have discussed both of them: Positive Reviews: Negative Reviews: Wholesale Options with Final Expense Network Wholesale options with this insurance company cater to brokers and agents seeking bulk final expense insurance solutions. These wholesale programs provide various benefits and opportunities for professionals in the insurance industry: 1- Discounted Rates Brokers and agents can access final expense insurance products at discounted wholesale rates, allowing them to offer competitive pricing to their clients. 2-

What Color Flowers For Funeral Are Used: A Complete Guide

What is the best way to honor and remember a loved one at their funeral? One timeless tradition is through the use of flowers. The “What Color Flowers For Funeral Are Used” can convey many emotions and messages, making your tribute beautiful and deeply meaningful. Each flower color carries its significance, from the purity and peace symbolized by white blooms to the respect and love conveyed by red ones. Understanding these meanings can help you select the perfect arrangement to express your sentiments and provide comfort during a difficult time. In this guide, we’ll find out what color flowers for funerals are used, their significance, and more helping you make the right choice for this solemn occasion. The Significance of Flowers at Funerals Flowers have been a part of funeral rituals for centuries. They hold deep significance, symbolizing love, respect, remembrance, and condolences for the deceased. They convey emotions that words often cannot express, offering comfort to grieving families. Each flower color carries a specific meaning, reflecting different sentiments and emotions. The presence of flowers creates a serene environment and helps honor the memory of the departed. Different cultures have specific flower traditions, but the universal purpose remains to provide solace and pay tribute. What Color Flowers For Funeral Are Used? Choosing the right color of flowers for a funeral is an important gesture of respect and sympathy. Each color has its meaning, helping to convey different sentiments. Here are some of the common flower colors used in the funeral along with their meanings: 1- White Flowers White flowers are the most traditional choice for funerals. They symbolize purity, innocence, and peace. White lilies, roses, and carnations are often used in funeral arrangements. These flowers convey a sense of serenity and hope, making them suitable for honoring the memory of the deceased. Popular White Flowers for Funerals: 2- Red Flowers Red flowers express love, respect, and courage. While not as common as white flowers, they are still appropriate for funerals, especially for close family members. Red roses, in particular, can signify the deep love and affection you had for the departed. Popular Red Flowers for Funerals: 3- Pink Flowers Pink flowers represent grace, compassion, and sympathy. They are a gentle way to express your condolences and can add a touch of warmth to a funeral arrangement. Pink carnations and roses are popular choices for expressing sympathy. Popular Pink Flowers for Funerals: 4- Yellow Flowers Yellow flowers symbolize friendship, joy, and new beginnings. While they are not traditionally used in funeral arrangements, they can be appropriate for celebrating the life of a vibrant and cheerful individual. They offer a more uplifting approach to expressing sympathy. Popular Yellow Flowers for Funerals: 5- Blue Flowers Blue flowers convey peace, calm, and serenity. They are a beautiful way to express your hope for peace and comfort for the grieving family. Blue delphiniums and hydrangeas are often chosen for their soothing qualities. Popular Blue Flowers for Funerals: 6- Purple Flowers Purple flowers symbolize dignity, respect, and admiration. They are often used in funeral arrangements to honor someone of high regard. Purple orchids and irises can convey a deep sense of respect and loss. Popular Purple Flowers for Funerals: Mixed Flower Arrangements Sometimes, a mixed flower arrangement is the best choice. Combining different colors and types of flowers can create a more personalized and meaningful tribute. For example, you might combine white lilies with red roses to signify both peace and deep love. Types of Funeral Flower Arrangements Choosing the right flower arrangement for a funeral is a meaningful way to honor the deceased and offer comfort to their loved ones. There are several types of funeral flower arrangements, each serving a unique purpose and placement during the service. Here are the most common types: Wreaths Wreaths are circular arrangements that symbolize eternal life and continuity. They are often placed on stands near the casket or at the gravesite. Common flowers used in wreaths include lilies, roses, and chrysanthemums. Sprays Sprays are large, flat arrangements displayed on an easel. They come in two main styles: Single-Ended Sprays: These have flowers concentrated at one end, often used for smaller spaces. Double-Ended Sprays: These have flowers arranged on both ends, suitable for larger displays and usually positioned near the casket. Bouquets Bouquets are smaller arrangements that can be placed on the casket, or gravesite, or given directly to the family. They offer a personal touch and can be customized to reflect the deceased’s personality and preferences. Baskets Flower baskets are versatile and can be placed anywhere in the funeral home, church, or gravesite. They are practical for those sending flowers from a distance and come in various sizes and styles, often featuring a mix of flowers to create a beautiful display. Casket Sprays Casket sprays are large arrangements placed directly on top of the casket. There are two main types: Full Casket Sprays: These cover the entire casket and are typically chosen for closed casket services. Half Casket Sprays: These cover only half of the casket and are suitable for open casket services. Inside Pieces Inside pieces are small floral arrangements placed inside the casket. These include mini bouquets, rosaries made of flowers, and floral pillows. Close family members often provide them as a final gesture of love and remembrance. Standing Arrangements Standing arrangements are displayed on easels and placed around the funeral venue. They are typically large and eye-catching, often featuring a mix of flowers to create a stunning tribute. These arrangements can include crosses, hearts, and other shapes that hold special meaning. What Color Flowers for Funeral Are Best? The most suitable flower colors for funerals are typically white, red, pink, and blue, each carrying its symbolic meaning. Here we discussed their different varieties in detail so you pick according to your choice: 1- White Flowers Lilies: Lilies, particularly white lilies like Easter lilies or Oriental lilies, symbolize purity, innocence, and the restored innocence of the soul. They are a traditional and elegant choice for

Prosperity Supplemental Insurance: Enhancing Coverage Option

Are you looking for ways to enhance your insurance coverage and protect yourself from unexpected expenses? Prosperity supplemental insurance might be the solution you’ve been searching for. Imagine having the satisfaction of knowing that you have additional financial protection in place, allowing you to focus on your health and recovery without the stress of high out-of-pocket costs. In this blog post, we’ll explore the benefits of Prosperity insurance and how it can enhance your coverage options. From hospital indemnity insurance to critical illness and accident insurance, Prosperity offers a range of options to suit your needs and budget. Let’s discover them. Understanding Supplemental Insurance Supplemental insurance is a type of insurance policy that helps cover the gaps in your primary health insurance coverage. It provides additional benefits for expenses that are not fully covered by your regular health insurance plan, such as deductibles, copayments, and coinsurance. Supplemental insurance can help protect you from high out-of-pocket costs and provide you with financial assistance when you need it most. There are several types of supplemental insurance policies available, including critical illness insurance, accident insurance, hospital indemnity insurance, and disability insurance. Each type of policy offers different benefits and coverage options, so it’s important to understand what each policy covers and how it can benefit you. Supplemental insurance policies are typically affordable and can provide you with added peace of mind knowing that you have extra protection in place. They can help ease the financial burden of unexpected medical expenses and allow you to focus on your recovery without worrying about the cost. What is Prosperity Supplemental Insurance? Prosperity supplemental insurance is a part of the broader offerings from Prosperity Life Group, which was founded in 2009. The group offers a variety of life insurance products across all 50 states and the District of Columbia. However, instead of issuing policies directly, Prosperity Life Group works with three issuing companies: S.USA, SBLI USA, and Shenandoah Life. Prosperity Insurance offers eight life insurance options, including Golden Promise Life Insurance, New Vista Whole Life Insurance, Legacy Benefit Individual Indexed Universal Life, Legacy Solution Single Premium Universal Life, SeniorLife Insurance, Family Freedom Term, PrimeTerm to 100 Life Insurance, and Simple Issue Term. Each option provides different benefits and coverage levels to suit individual needs. Benefits of Prosperity Supplemental Insurance Prosperity supplemental insurance offers a range of benefits that can provide you with added financial protection and peace of mind. Here are some key benefits of this insurance: Financial Protection Prosperity insurance provides an additional layer of financial security, ensuring that you’re not left with high out-of-pocket costs in the event of an unexpected illness or injury. Enhanced Coverage By adding this insurance plan to your existing policy, you can enhance your coverage without having to switch plans or providers. Peace of Mind Knowing that you have additional coverage in place can provide peace of mind, allowing you to focus on your health and recovery. Flexibility Prosperity offers a variety of supplemental insurance options, allowing you to choose the coverage that best suits your needs and budget. Customizable Coverage With this insurance plan, you can customize your coverage to include benefits that are most important to you, such as hospital indemnity, critical illness, accident, or disability insurance. Affordability Supplemental insurance policies are typically affordable, making it easy to add extra protection to your existing coverage without breaking the bank. Overall, Prosperity supplemental insurance can provide you with the added security and flexibility you need to face life’s uncertainties with confidence. Types of Prosperity Supplemental Insurance Prosperity supplemental insurance offers a variety of options to enhance your coverage and protect you from unexpected expenses. Here are some of the types of Prosperity insurance available: 1- Hospital Indemnity Insurance This type of insurance provides a lump-sum payment if you are hospitalized, helping to cover expenses not covered by your primary insurance, such as deductibles, copayments, and other out-of-pocket costs. 2- Critical Illness Insurance Critical illness insurance provides a lump-sum payment if you are diagnosed with a covered illness, such as cancer, heart attack, or stroke. This payment can help cover medical expenses and other costs associated with your illness. 3- Accident Insurance Accident insurance provides a lump-sum payment if you are injured in an accident, helping to cover medical expenses and other costs related to your injury, such as lost wages or transportation expenses. 4- Disability Insurance Disability insurance provides income replacement if you are unable to work due to a covered illness or injury. This can help cover your living expenses while you are unable to work. Each type of Prosperity insurance offers different benefits and coverage options, allowing you to choose the coverage that best suits your needs and budget. Contact a Prosperity insurance agent to learn more about the types of supplemental insurance available and how they can enhance your coverage options. Cost of Prosperity Supplemental Insurance To provide accurate cost information for Prosperity insurance, we would need specific details about the type of coverage you’re interested in, your age, health status, and other factors that can affect the premium. However, here is a general idea of the cost range for different types of supplemental insurance policies offered by Prosperity. Type of Supplemental Insurance Estimated Monthly Premium Range Hospital Indemnity Insurance $30 – $100 Critical Illness Insurance $25 – $80 Accident Insurance $20 – $60 Disability Insurance $30 – $100 These estimates are based on average premiums and may vary based on individual factors. For a more accurate quote, it’s best to contact Prosperity directly or speak with an insurance agent who can provide personalized pricing based on your specific needs. How to Get Prosperity Supplemental Insurance? Getting Prosperity insurance is straightforward. Here’s a step-by-step guide to help you get started: 1- Research Your Options Take some time to research the different types of supplemental insurance available and determine which ones best fit your needs and budget. 2- Contact an Insurance Agent Once you’ve decided on the type of supplemental insurance you want, contact a Prosperity

Old Mutual Funeral Policy: Easy Claims & Comprehensive Cover

Have you ever wondered how you can ensure your loved ones aren’t burdened with unexpected expenses when you’re no longer around? The Old Mutual Funeral Policy might be the answer you’re looking for. This policy offers peace of mind with its straightforward claims process and extensive coverage options. Old Mutual, a trusted name in the insurance industry with over 75 years of experience, provides a range of plans tailored to meet various needs and budgets. In this blog post, we’ll explore the benefits, coverage details, and the easy claims process of the Old Mutual Funeral Policy. By the end, you’ll understand why this policy is a valuable choice for protecting your family’s financial future during one of life’s most challenging times. What is the Old Mutual Funeral Policy? The Old Mutual Funeral Policy is an insurance plan designed to cover the costs associated with funerals. This policy ensures that when the policyholder passes away, their family doesn’t have to bear the financial burden of funeral expenses. It offers comprehensive coverage, including costs for the funeral service, casket, transport, burial or cremation, and related ceremonial expenses. Old Mutual, a well-established and trusted insurance provider with years of experience, offers this policy to provide peace of mind and financial security. The policy includes flexible plans to suit various needs and budgets, additional benefits like accidental death cover and memorial benefits, and options to cover family members. How Does Old Mutual Funeral Policy Work? The Old Mutual Funeral Plan is designed to provide financial support for funeral expenses, ensuring that your loved ones are not burdened during an already difficult time. Here’s how it works: 1. Application Process 2. Premium Payments 3. Coverage Provided 4. Claims Process 5. Ongoing Policy Management The Old Mutual Funeral Plan is structured to offer ease and flexibility, ensuring that policyholders and their families have the financial support they need during a challenging time. With its comprehensive coverage and efficient claims process, it provides peace of mind and security for the future. What are the Plans of Old Mutual Funeral Policy? Old Mutual offers several funeral policy plans, each tailored to meet different needs and budgets. These plans ensure that you can find a suitable option that provides the necessary coverage for you and your loved ones. Here’s an overview of the main plans available: Basic Funeral Plan The Basic Funeral Plan is the most affordable option offered by Old Mutual. It provides essential coverage for those on a tighter budget. This plan focuses on covering the core expenses of a funeral, such as the cost of the casket or coffin and the burial or cremation fees. Additionally, the claims process is straightforward and designed to ensure rapid payout, which is crucial for covering funeral expenses promptly. Standard Funeral Plan The Standard Funeral Plan offers more extensive coverage compared to the basic plan. It not only covers the essential funeral service costs but also includes additional expenses that might arise. This plan is ideal for those who want a bit more comprehensive coverage. Moreover, this plan also provides flexible payment options, allowing you to choose a premium payment schedule; whether monthly, quarterly, or annually, that best fits your financial situation. Family Funeral Plan The Family Funeral Plan is designed to provide inclusive coverage for the policyholder and their immediate family including the spouse, children, and even parents. Along with usual funeral expenses, this plan often includes an accidental death benefit, which provides an extra payout in case of accidental death. Another attractive feature it is the cashback benefit, which rewards policyholders with a portion of their premiums after a specified period, providing additional financial benefits. Premium Funeral Plan The Premium Funeral Plan offers the highest level of coverage among Old Mutual’s funeral policies. It includes all the benefits of the Standard Plan but with added features and higher payouts. This plan ensures that every aspect of the funeral and related expenses is covered extensively. The memorial benefit included in this plan is particularly comprehensive, covering the costs of a tombstone or memorial service to ensure a dignified farewell. Customized Plans For those with specific needs or preferences, Old Mutual provides the option of Customized Plans. These plans are tailored to meet unique requirements, allowing policyholders to choose the exact coverage and benefits they need. This flexibility means you can adjust the plan as your circumstances change, ensuring continuous, appropriate coverage. These plans provide a personalized approach to funeral insurance, ensuring that every detail aligns with your individual or family needs. Benefits of Old Mutual Funeral Policy The Old Mutual Funeral Plan offers a range of benefits designed to provide peace of mind and financial security for you and your loved ones. Here are some key benefits of the policy: Flexible Plans Old Mutual offers flexible plans to suit different needs and budgets. Whether you’re looking for a basic plan or a more extensive cover, there is an option for you. You can also adjust your plan as your circumstances change, ensuring that you always have the appropriate level of coverage. Easy Claims Process The claims process for the Old Mutual Funeral Plan is straightforward and hassle-free. In the event of a claim, the process is quick, with most claims settled within 48 hours. This rapid response helps your family manage immediate expenses without additional stress. Additional Benefits Depending on the plan you choose, the Old Mutual Funeral Policy may include additional benefits such as accidental death cover, memorial benefits for tombstone or memorial service costs, and cashback options. These additional benefits provide extra financial support and rewards for maintaining your policy. Family Cover You can extend your Old Mutual Funeral Plan to cover your immediate family, including your spouse, children, and even parents. This extension ensures that your entire family is protected under one plan, simplifying management and providing peace of mind. Affordable Premiums Old Mutual offers competitive premiums that provide value for money. You can choose a payment frequency that suits your budget, whether it’s monthly,

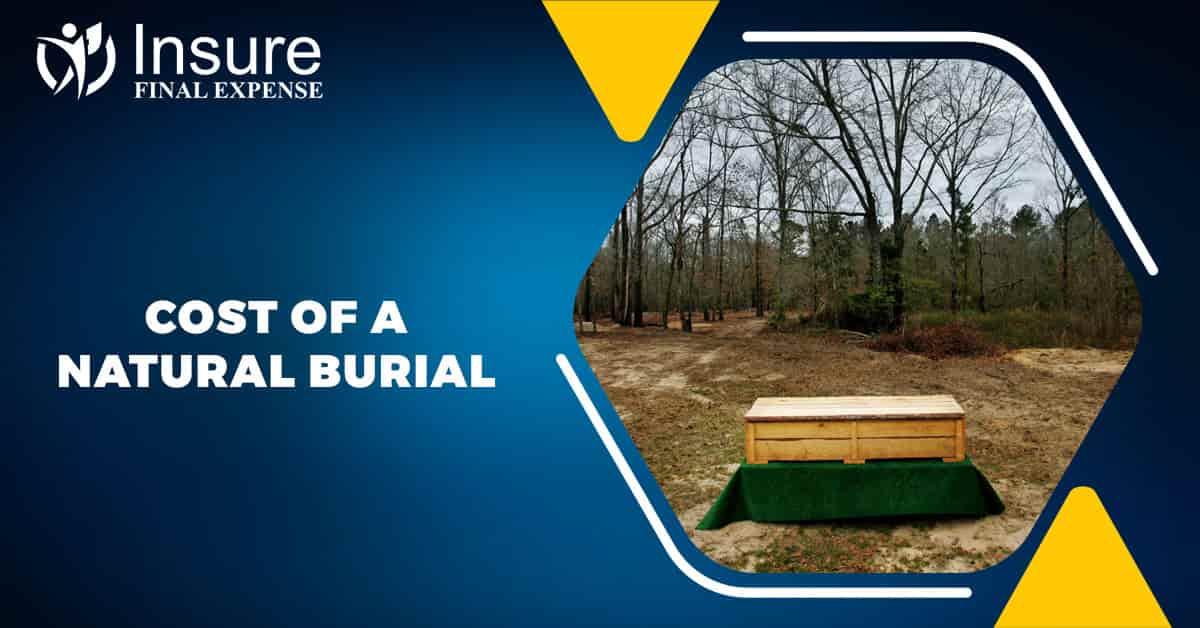

The Cost of a Natural Burial: What You Need to Know

Are you interested in ways to memorialize someone while also preserving the planet? Natural burials are becoming more common as people opt for eco-friendly funeral services that are gentle on the environment. But what is the cost of a natural burial? We have got you. In this blog post, we will explore various factors influencing the natural burial cost and how much generally it costs in the USA. What is a Natural Burial? A green funeral or natural burial is a biodegradable funeral that is friendly to nature to avoid polluting the ecosystem. The purpose of environmental management is to reduce any action that can cause harm to the planet. Here are the key aspects of a natural burial: What is the Cost of a Natural Burial? Different factors determine the cost of a natural burial. These may include if you prefer to have a funeral or an open viewing, the location of the burial, and other services. Some services and costs are not included in green burials. For example, there is no need for embalming and casket treatment. This makes green burial a cheaper option. They can be less expensive than the average $2,597 for a standard funeral or $9,420 for a traditional burial. Average Cost of a Natural Burial A natural burial costs less than an average burial, and the price ranges from $1,000 to $4,000. Let’s break this down: 1- Burial Plot The costs of burial cemeteries that have natural grounds range between $500 and $2000. The price of caskets is determined by the geographic area and the rules and regulations of the cemetery. However, prices might be lower in rural areas as compared to urban areas. 2- Casket The price of a biodegradable casket ranges from $200 to 1,500 dollars. Some of the common choices for constructing the casket are wicker, cardboard, and untreated wood. Some may also go for a shroud and this may be cheaper for them as compared to other accessories. 3- Grave Marker Natural markers are inexpensive. For instance, an inexpensive grave marker may just be a stone or a wooden plate that may be over $50 and go up to $ 200. Some even make no allowance for tombstones with restrictions that only flat stones or plants should be used. 4- Additional Services These services may include body preparation, transportation, and ceremonies which further expand the charges. The on-guard services generally include the package services which may cost anything between $300 to $1500. Cost Comparison Between Natural and Traditional Burials Natural burials are usually lower as compared to traditional burials as they don’t involve certain services. Here is a cost breakdown of both burials to get an estimate: Services/Products Green Burial Cost Direct Burial Cost Remains removal/transfer $350 $350 Burial permit $10-$30 $10-$30 Casket $0-$1,500 $2,500-$3,000 Cemetery plot $3,581 $3,581 Grave liner $0 $750-$1,000 Grave marker $100 $2,000 What are the Benefits of Natural Burials? Natural or green burials offer several benefits for you as well as our environment. Here are some of the key benefits: 1- Environmental Impact Natural burials minimize the use of dangerous chemicals that can pollute both soil and groundwater systems by seeping. Moreover, they also reduce the amount of carbon dioxide emitted to the atmosphere through the manufacturing of conventional caskets and vaults. 2- Cost-Effectiveness Compared to the traditional burial services that require such accessories as expensive caskets and burial vaults and the need to embalm a body, green burials are relatively cheaper. It can help alleviate some financial burdens, especially in a period of crisis. 3- Personalization Similar to other burials, green burial gives the families a chance to develop ceremonies that befit the deceased’s life and spirit. It can bring comfort and determination to the family members who are grieving the death of their loved ones. 4- Community Support Going for a natural burial also ensures that the burying requirements do not disturb the ecosystems by preserving novel natural landscapes. The reserved graves for those who want an environmentally friendly funeral become homes to wildlife hence enhancing the bio-diversity. 5- Simplicity and Peace The reason, green burial can be seen as a simple activity that at the same time can help to bring peace to the dead person and the ones close to them. It also helps do away with the complex and sometimes stressful funeral plans that are otherwise needed when a body is sick. 6- Alignment with Values People opt for natural burials in the same way that they choose their lifestyles, to suit their beliefs and philosophy on sustainable living. This decision can also give a purpose and certain satisfaction to the person taking it consolation. Alternatives to Natural Burials Although natural burial seems to be a perfect choice for lovers of green burial, several other options are also environment-friendly. Here are some options: The Bottom Line The cost of a natural burial is lower as compared to conventional burial methods and it is also environmentally friendly. They cost between $1,000 and $4,000 which makes them cheaper, easier and environmentally friendly than traditional burial. Still, learning cost factors helps in making the core, proper decisions for yourself. It is important to choose a burial that reflects your values and is also affordable. Frequently Asked Questions (FAQs)

Attorney for Death Benefits: Ensuring Your Rights & Benefits

Have you ever wondered how to navigate the complexities of death benefits after losing a loved one? Dealing with the aftershock of a loss is never easy, and the financial and legal processes can add to the stress. Death benefits, which include life insurance payouts, pensions, Social Security, and worker’s compensation, are meant to provide crucial financial support. However, claiming these benefits can often be challenging and confusing. This is where an attorney for death benefits can make a significant difference. They offer expertise, handle paperwork, resolve disputes, and ensure you receive everything you’re entitled to. In this blog post, we’ll explore why hiring an attorney for death benefits is essential and how they can help you during this difficult time. Let’s get started! What are Death Benefits? Death benefits are financial payments or benefits provided to the beneficiaries of a deceased individual. These benefits are typically paid out by various entities such as life insurance companies, pension plans, Social Security Administration, and worker’s compensation programs. The purpose of death benefits is to provide financial support to the surviving family members or dependents of the deceased to help them manage the financial impact of the loss. The types and amount of death benefits vary depending on the specific circumstances and the policies of the entity providing the benefits. For example, life insurance policies often pay out a lump sum to the designated beneficiaries, while pension plans may offer survivor benefits to the spouse or dependents of the deceased. Why Do You Need an Attorney for Death Benefits? Exploring the complexities of death benefits can be overwhelming, especially during a time of grief. Here’s why having an attorney for death benefits can make a significant difference: Attorneys specializing in death benefits understand the intricate legal processes involved. They can interpret complex laws and regulations, ensuring your claim is handled correctly. Filing for death benefits requires extensive documentation. An attorney can assist in completing and submitting all necessary paperwork accurately, minimizing the risk of delays or denials. In cases where claims are denied or disputed, an attorney can advocate on your behalf. They can challenge wrongful denials and negotiate with insurance companies or other entities to secure the benefits you’re entitled to. An attorney can help you identify all available benefits and ensure you claim everything you’re entitled to. This can maximize your financial support during a difficult time. What is the Process of Working with an Attorney for Death Benefits? Working with an attorney for death benefits typically involves several key steps: 1- Initial Consultation The process begins with an initial consultation with the attorney. During this meeting, you’ll discuss your case, provide relevant information about the deceased and the benefits you’re seeking, and ask any questions you may have. 2- Case Evaluation After the consultation, the attorney will evaluate your case. They’ll review the details you provided, assess the strength of your claim, and determine the best course of action. 3- Filing the Claim If you decide to move forward, the attorney will help you gather the necessary documents and information needed to file your claim. They’ll ensure all paperwork is completed accurately and submitted on time. 4- Negotiation and Dispute Resolution If there are any disputes or negotiations required, your attorney will handle them on your behalf. They’ll communicate with insurance companies, pension administrators, or other entities to resolve any issues and secure your benefits. 5- Continuous Support Throughout the process, your attorney will provide ongoing support and guidance. They’ll keep you informed about the progress of your case, answer any questions you may have, and advocate for your best interests. By working closely with an attorney experienced in death benefits, you can confidently navigate the process’s complexities, knowing that your legal rights are protected, and you’re receiving the full benefits you’re entitled to. How To Claim Death Benefits After The Loss Of A Loved One? Claiming death benefits after the loss of a loved one can be a complex process, but it’s essential to ensure you receive the financial support you’re entitled to. Here’s a general guide on how to claim death benefits: Gather Documentation: Collect all necessary documents related to the deceased, including their death certificate, social security number, insurance policies, and any other relevant paperwork. Contact Relevant Entities: Reach out to the appropriate entities that provide death benefits, such as life insurance companies, pension administrators, Social Security Administration, or worker’s compensation programs. Notify them of the death and inquire about the process for filing a claim. Complete Forms: Fill out any required claim forms provided by the entities. Make sure to provide accurate and thorough information to avoid delays or complications in processing your claim. Submit Documentation: Along with the completed forms, submit all necessary documentation, including the death certificate and any other requested paperwork. Keep copies of everything for your records. Follow-up: Stay in touch with the entities processing your claim to ensure everything is progressing smoothly. Be proactive in providing any additional information or documentation they may request. Seek Legal Assistance if Needed: If you encounter difficulties or disputes with your claim, consider seeking assistance from an attorney who specializes in death benefits. They can provide guidance, advocate on your behalf, and help resolve any issues that arise. Monitor Payments: Once your claim is approved, monitor payments closely to ensure you receive the correct amount on time. Contact the entity immediately if you notice any discrepancies or delays. By following these steps and seeking assistance when needed, you can claim death benefits after the loss of a loved one and secure the financial support you and your family need during this challenging time. Common Challenges in Claiming Death Benefits Claiming death benefits can be a complex process, and several common challenges can arise. Here are some of the most common challenges you may encounter when claiming death benefits: One of the most common challenges is submitting incomplete or inaccurate documentation. This can lead to delays or denials of your claim. Make sure to